Table of Contents

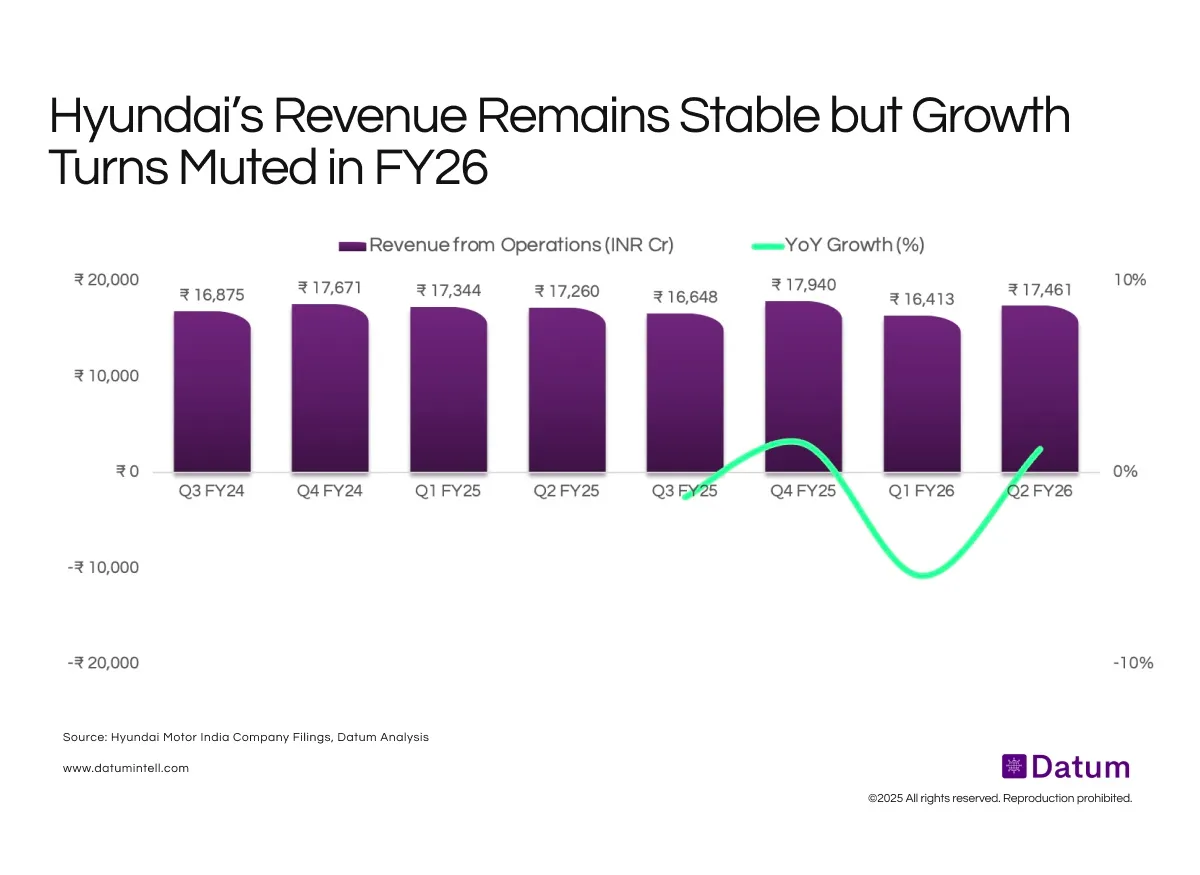

Hyundai Motor India (HMI) delivered a stable Q2FY26 performance with modest topline growth despite domestic headwinds. Revenue grew 1.2% YoY to ₹174bn, supported by higher ASPs, strong export traction, and robust festive demand. The company is navigating an evolving mix shift, rising rural penetration, and new model launches, while preparing for near-term margin pressure from the new Pune plant ramp-up.

Demand & Growth

- Revenue grew 1.2% YoY in Q2FY26, supported by a 1.7% ASP uplift and 29.5% export revenue growth, which offset a 6.7% decline in domestic revenue.

- Festive retails (22 Sep–23 Oct 2025) rose 23% YoY, with broad-based strength across segments:

- Hatchbacks +16%, Sedans +47%, SUVs +21%.

- Exter and Venue volumes grew 28%, reinforcing Hyundai’s leadership in sub-compact and compact SUVs.

Portfolio Mix & Market Position

- SUV penetration reached a record 71%, reflecting continued mix premiumisation.

- Rural penetration improved to 23.6%, up from 22.6% in Q1FY26 and 20.9% in FY25 — signalling deeper market penetration outside metros.

- First-time buyers contributed ~40% of sales, up from 32% in FY20, highlighting structural expansion of the addressable market.

What It Means

Hyundai’s fundamentals remain resilient. Even with a 7% YoY decline in domestic volumes, stronger exports (+22%), rising ASPs (+1.7%), and a strong festive cycle kept revenue stable. Structural tailwinds-SUV leadership, deepening rural penetration, and higher first-time buyer contribution—point to sustained demand momentum. However, margin gains could moderate as Pune plant costs scale up, placing greater emphasis on mix improvement and the New Venue as a key catalyst to absorb incremental overheads.

{kind=link}