Table of Contents

Korean noodles now account for 34% of all noodle sales on Blinkit across India's top 30 cities.

But here's the real story: Two Korean brands—Nongshim and Samyang—together control 24% of the entire instant noodles category. That's nearly one in four noodle purchases on India's fastest-growing grocery platform.

The brand breakdown:

- Nongshim: 44% of Korean noodles market → 14.9% of total noodles

- Samyang: 27.2% of Korean noodles → 9.2% of total noodles

- Maggi: Still leads at 34.7%, but only 5.4% of its portfolio is Korean variants

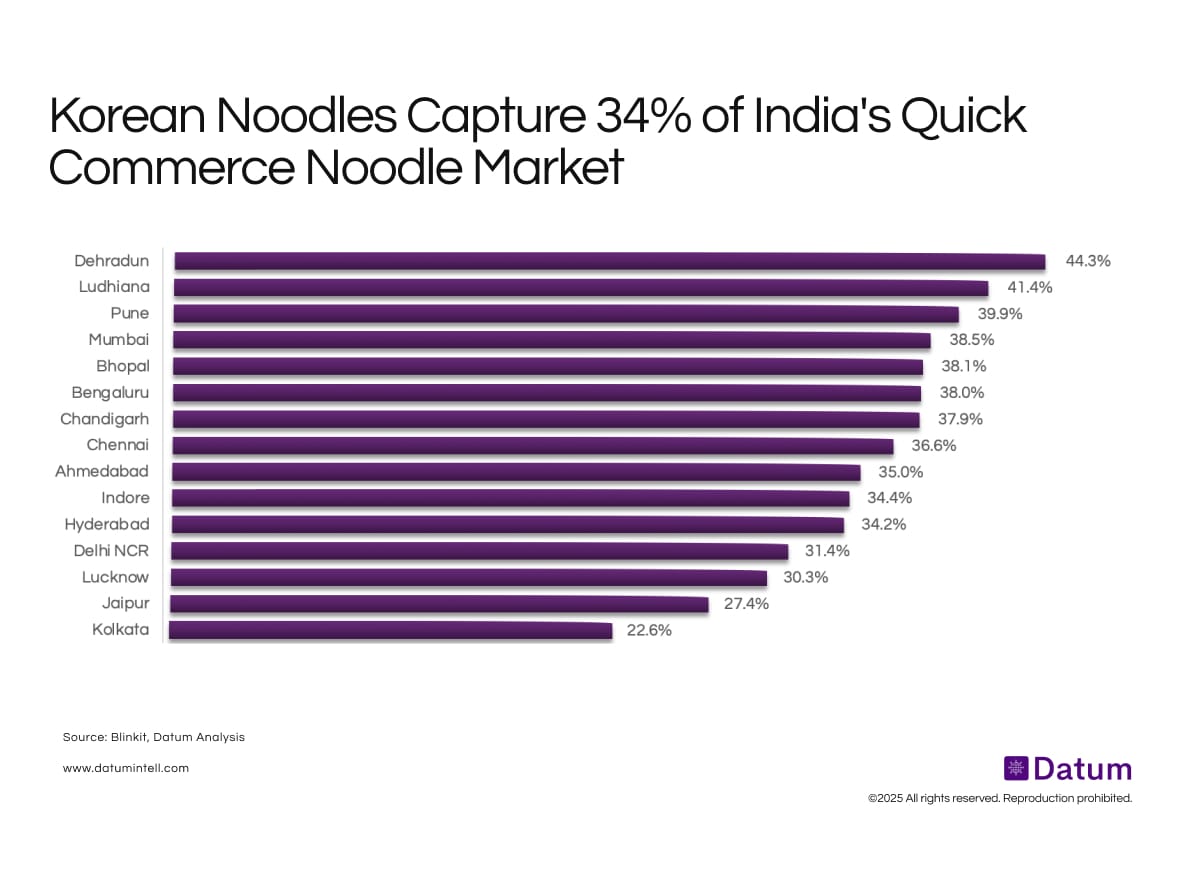

In less than three years, Korean noodles have captured nearly half the quick commerce noodle market in cities like Dehradun (44.3%), Ludhiana (41.4%), and Pune (39.9%).

Even metros aren't far behind: Mumbai (38.5%), Bengaluru (38.0%), and Chennai (36.6%) show massive adoption.

The Tier-2 Surprise

The conventional wisdom is wrong. Global food trends don't trickle down from metros to Tier-2 cities—they're moving simultaneously, sometimes even faster in smaller cities.

Top 5 markets for Korean noodles on Blinkit:

- Dehradun – 44.3%

- Ludhiana – 41.4%

- Pune – 39.9%

- Mumbai – 38.5%

- Bhopal – 38.1%

Three of the top five are Tier-2 cities. Delhi NCR (31.4%) and Kolkata (22.6%) actually lag behind.

Why? Tier-2 consumers have:

- High cultural receptivity (K-dramas, K-pop on OTT)

- Lower dining-out options (global cuisines harder to access)

- Strong quick commerce penetration (Blinkit, Zepto expansion)

- Younger demographics experimenting with food

The Brand Battle: Pure-Play Korean vs. Everyone Else

The data reveals three distinct strategies:

- Pure-Play Korean Dominators. Brands selling 100% Korean-style noodles:

- Nongshim (14.9% total market share) – The undisputed leader

- Samyang (9.2%) – Known for viral "fire noodles" challenge

- Ottogi (0.9%) – Premium positioning

- YOPOKKI, Jify, Baeku – Emerging niche players

Combined Korean pure-play brands: ~25% of total noodles market

- Hybrid Players Hedging Bets. Legacy brands adding Korean variants to their portfolio:

- Nissin: 50.7% of sales now Korean-style (6.5% total market)

- Knorr: 64% Korean variants (0.7% total market)

- Yu Noodles: 49% Korean (4.4% total market)

These brands are betting both ways—keeping traditional offerings while capturing Korean demand.

- The Maggi Problem. Maggi still commands 34.7% of the instant noodles category, but:

- Only 5.4% of Maggi's sales are Korean variants

- Its core ₹12-20 Masala/Atta noodles face margin pressure

- Korean brands are winning the ₹60-150 premium segment Maggi never owned

What's Driving This?

This repor t by kindlife x Datum offers a comprehensive analysis of the market dynamics, consumer expectations, and key trends shaping the K-beauty landscape in India in .

- The Hallyu Wave Meets 10-Minute Delivery. K-content consumption has exploded: Korean dramas on Netflix, K-pop on YouTube, Korean skincare routines on Instagram. Food follows content. When fans see characters eating ramyeon in Squid Game or Crash Landing on You, they want to try it—and Blinkit delivers it in 10 minutes.

- Premiumization Without Intimidation. Korean noodles sit at the sweet spot: ₹60-150 vs ₹12-20 for Maggi. Premium enough to feel aspirational, affordable enough for impulse. No restaurant visit needed, no cooking skill required—just add hot water.

- Flavor Fatigue. After decades of Maggi masala, Indian consumers are ready for bold new flavors. Korean noodles deliver: spicy, tangy, umami-rich, with chewy textures that feel different. Variety without complexity.

- Quick Commerce as Cultural Accelerant. Before Blinkit/Zepto, Korean noodles were niche—found only in specialty stores or expensive imports. Quick commerce democratized access. Now a college student in Bhopal can order Samyang Buldak as easily as someone in Bandra.

What This Means

For FMCG Brands:

- The ₹12 Maggi model is under threat from ₹100 premium alternatives

- Korean brands (Samyang, Nongshim, Ottogi) are capturing high-value consumers

- ITC, Nestle, HUL need to respond: launch premium SKUs, bold flavors, or acquire Korean brands

For Quick Commerce:

- Discovery drives conversion: Korean noodles succeed because apps surface them in recommendations, combos, and themed collections

- Inventory risk pays off: Stocking 15+ Korean SKU variants seems excessive—until they hit 40% category share

- Cultural merchandising matters: Pairing Korean noodles with Korean snacks, drinks, and sauces creates basket expansion

For Korean Brands:

This is a land grab moment.

- Nongshim at 14.9% can double to 30%+ before hitting saturation

- New Korean entrants have a 24-month window before Indian copycats flood the market

- Distribution partnerships with Blinkit/Zepto worth more than traditional retail expansion

- Localization not required yet—authenticity is the selling point

The Maggi Question

Maggi's 34.7% market share looks safe—until you zoom in.

Maggi's problem:

- It owns the ₹12-20 mass segment (still huge volume)

- But it's absent from the ₹60-150 premium segment where Korean brands print money

- Only 5.4% of Maggi sales are Korean variants (vs 100% for Nongshim/Samyang)

- Quick commerce consumers skew affluent—exactly the cohort trading up

Maggi's options:

- Launch aggressively priced Korean SKUs (₹40-50) to bridge the gap

- Acquire a Korean brand/distributor for instant credibility

- Defend mass market, cede premium (dangerous long-term)

- Create a new sub-brand (avoid diluting Maggi equity)

If Nestle waits 18 months, Korean brands will be too entrenched to dislodge.

We decode how Indian consumers discover, decide, and transact. For custom research on quick commerce, food trends, or category disruption, reach out at hello@datumintelligence.com