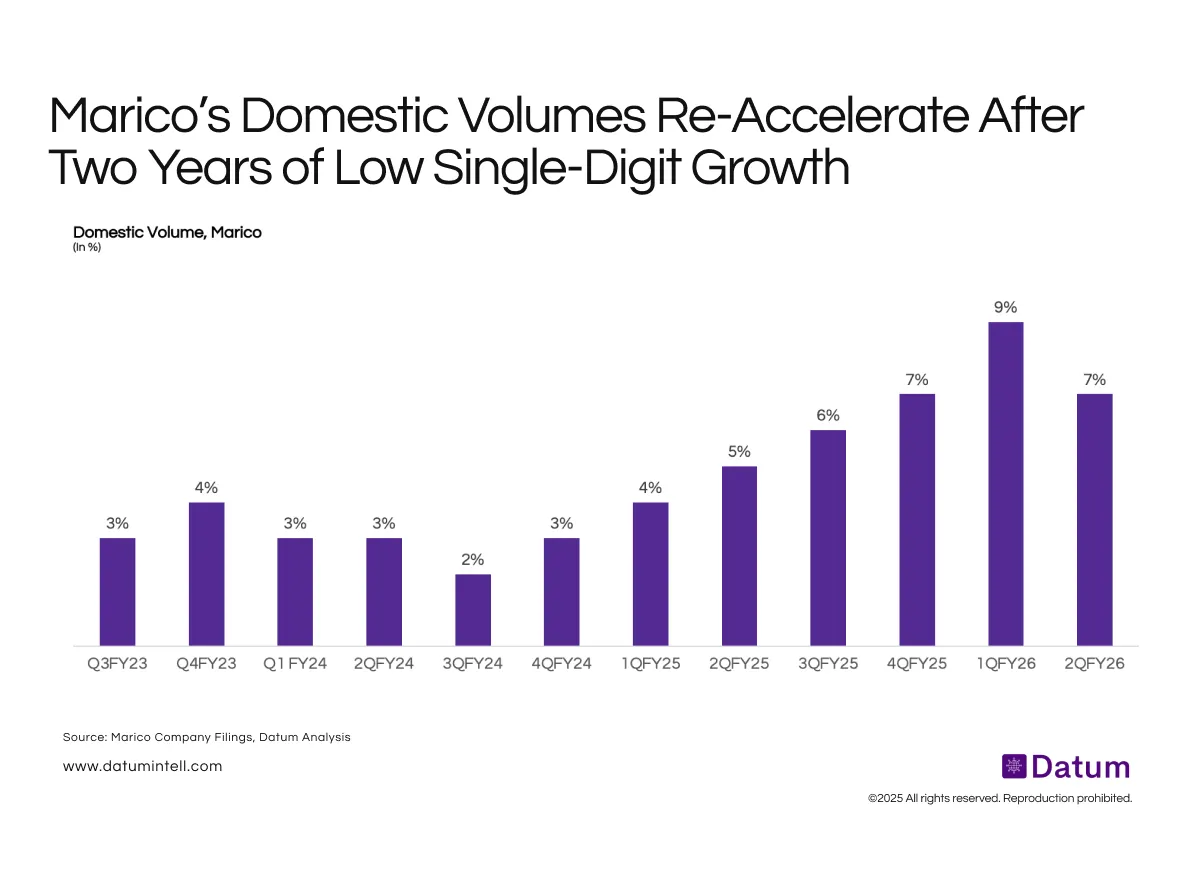

Domestic Volumes Recover Gradually, Reaching Their Strongest Levels in FY26 For Marico

Marico’s move from low single-digit to 7–9% domestic volume growth marks a clear inflection, driven by rural revival, portfolio strengthening, and improving category dynamics.