Table of Contents

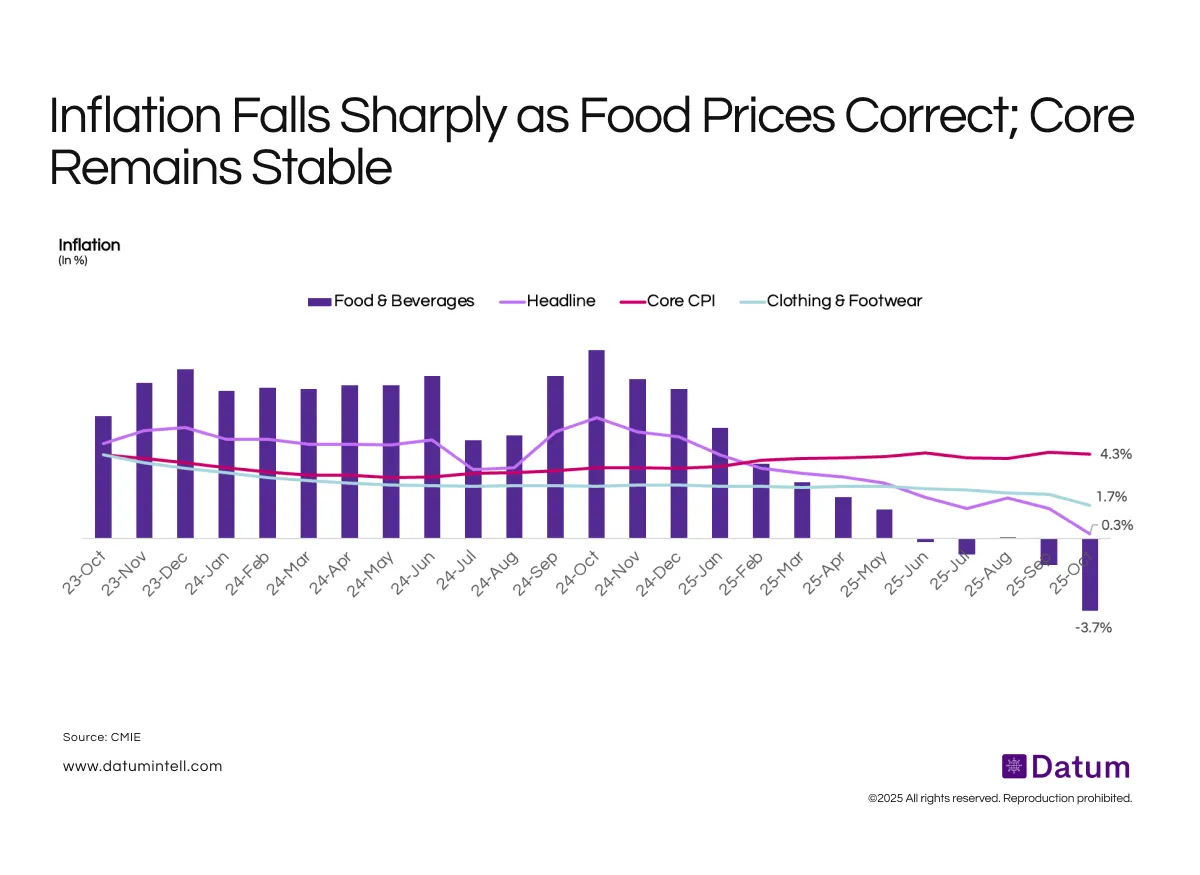

India’s inflation trajectory has softened meaningfully over the past year. Headline CPI has declined from above 6% in late 2023 to almost zero by Oct’25, driven primarily by a deep correction in food and beverage inflation, which has moved from high single digits to -3.7%. Clothing and footwear inflation has eased gradually, while core CPI has remained anchored in the 4–4.3% range, indicating stable underlying demand conditions. This combination of food disinflation, muted fuel prices, and steady core has produced one of the most benign inflation prints in recent years.

What It Means

The price environment has turned significantly more favourable, easing pressure on households and lifting real purchasing power. With food inflation in deflation and fuel costs subdued, monetary policy can remain supportive of growth. Stable core readings confirm the absence of demand-side overheating, reinforcing a constructive outlook for consumption and macro stability in FY26.

{kind=link}