Table of Contents

Flipkart’s Big Billion Days and Amazon’s Great Indian Festival are expected to return in 2025 with even greater scale and ambition. Both events are likely to begin in the second week of September and run through the last week of October, strategically covering the festive build-up to Diwali. Over the years, these sales have evolved into cultural touchpoints - driving record-breaking order volumes, surging app downloads, and becoming critical levers for new user acquisition and category expansion in India’s e-commerce landscape.

Consumer Sentiment Rebounds Across Urban and Rural India

Urban and rural India are showing strong signs of consumption revival ahead of the 2025 festive season.

- Urban sentiment turned net positive (+0.4) for the first time since 2022, with a sharp rise in discretionary spending (37.6% vs 27.8% in May).

- Rural confidence surged higher, with 54.7% reporting increased non-essential spend and net response hitting +37.2—the highest on record.

- Future outlook remains bullish across both segments, with 73.6% of rural and 43.6% of urban consumersexpecting to spend more in the next 12 months.

Card Payments on Ecommerce Rebound Sharply in Q2 2025 After Two Soft Years

After a brief decline in October–November 2024, credit and debit card spending on eCommerce rebounded strongly, growing ~20% YoY in March 2025 and maintaining double-digit momentum into Q1 FY26.

- April 2025 saw 18.4% YoY growth, almost doubling from 10.6% in April 2024 and surpassing even 2023 (12.9%).

- 2024 Was a Low Base Year. 2024 saw weakened card growth due to rising UPI dominance, reduced discretionary spending, and inflation-related caution especially in May–June, which recorded 7.4% and 7.1% growth respectively.

- With GST cuts expected soon and ecommerce platforms gearing up for early festive rollouts, H2 2025 could accelerate further on top of this solid Q1 base.

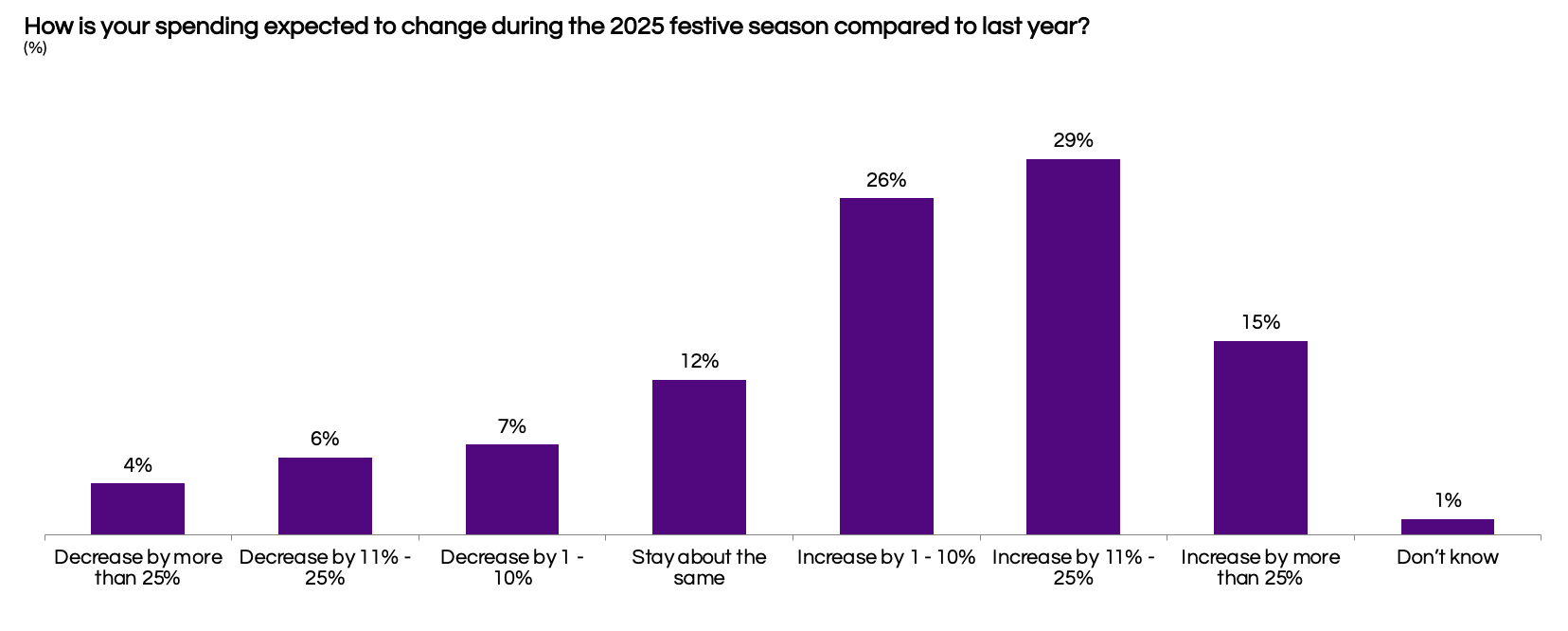

70% Buyers Are Expected to Increase Spending As Compared to 2024

Consumer sentiment ahead of the 2025 festive season points to strong momentum in discretionary spending. Nearly 70% of surveyed shoppers expect to spend more than they did in 2024, with 29% projecting an increase between 11% and 25%, and another 26% anticipating a more modest 1% to 10% rise. Additionally, 15% of consumers are planning a significant spike of over 25% in their festive spending. In contrast, only 17% expect any reduction in expenditure, while 12% intend to keep their spending at similar levels to last year.

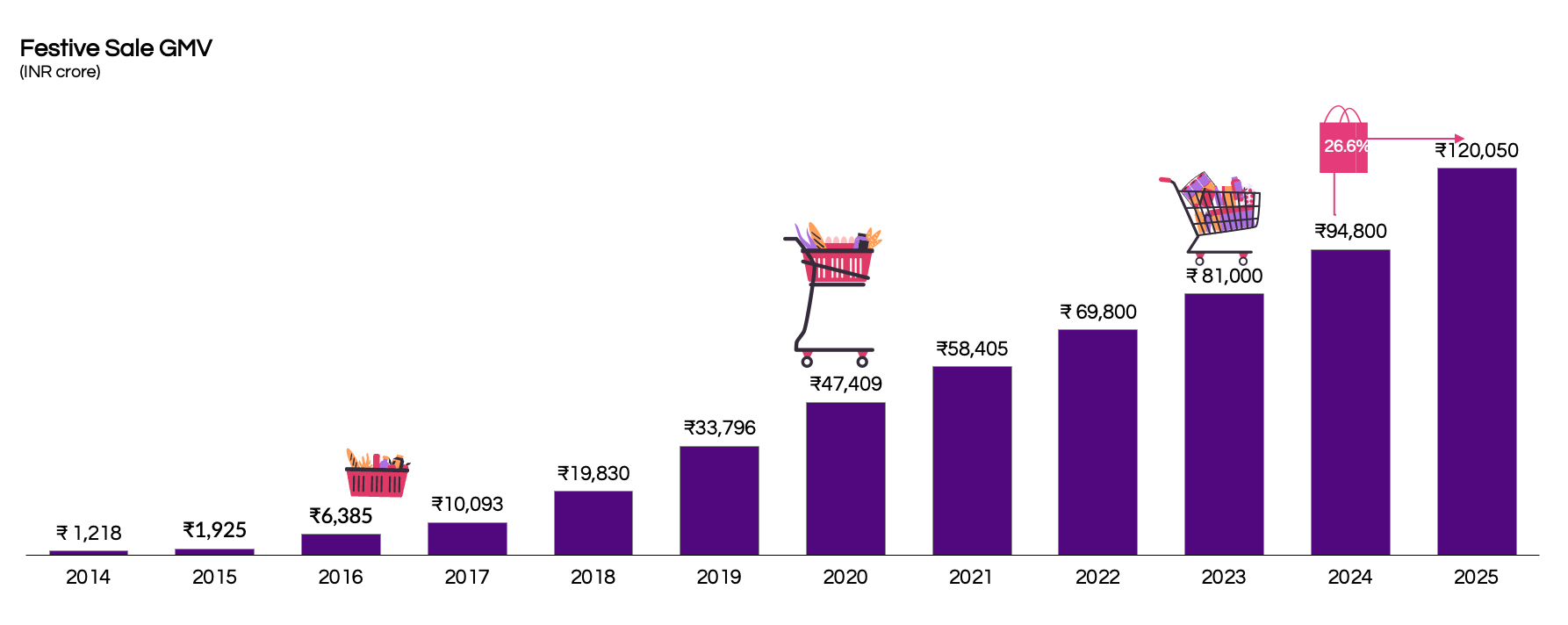

Festive Season Sales to Increase by 27% to Cross INR 120,000+ Crore

In 2025, festive sales are projected to hit ₹1.2 lakh crore ($13.9 billion), marking a 27% YoY growth over 2024. This reinforces the decade-long momentum in India’s festive e-commerce market, continuing a consistent upward trajectory since 2014.

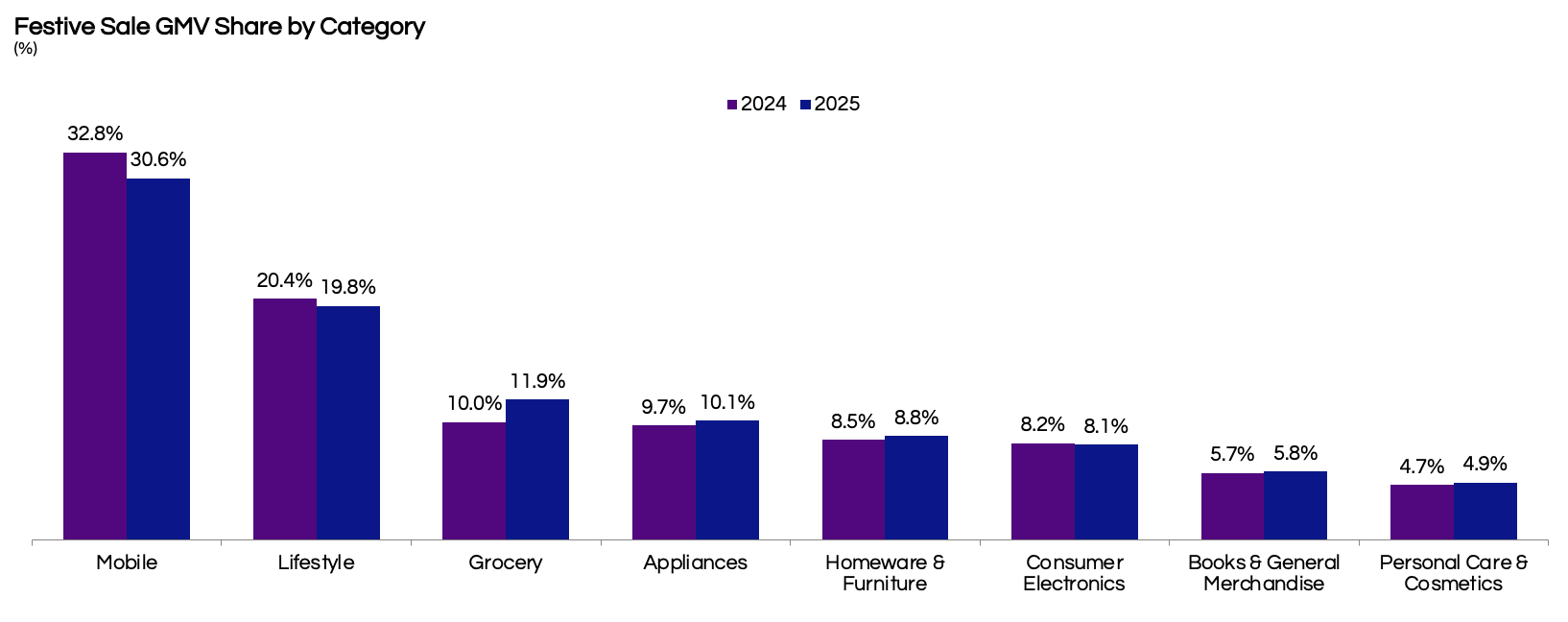

Mobile and Lifestyle Accounted for ~51% of Spending

In the 2025 festive season, mobile and lifestyle categories are expected to continue dominating online festive sales, together accounting for just over 50% of the total GMV. However, both have seen a slight dip in their share compared to 2024—mobiles declining from 32.8% to 30.6%, and lifestyle from 20.4% to 19.8%—indicating early signs of market diversification.

At the same time, grocery (rising to 11.9%), appliances, and personal care & cosmetics have gained share, driven by a growing preference for value-led, everyday essentials. This shift reflects the evolving festive basket, with consumers expanding their spend beyond traditional big-ticket items.

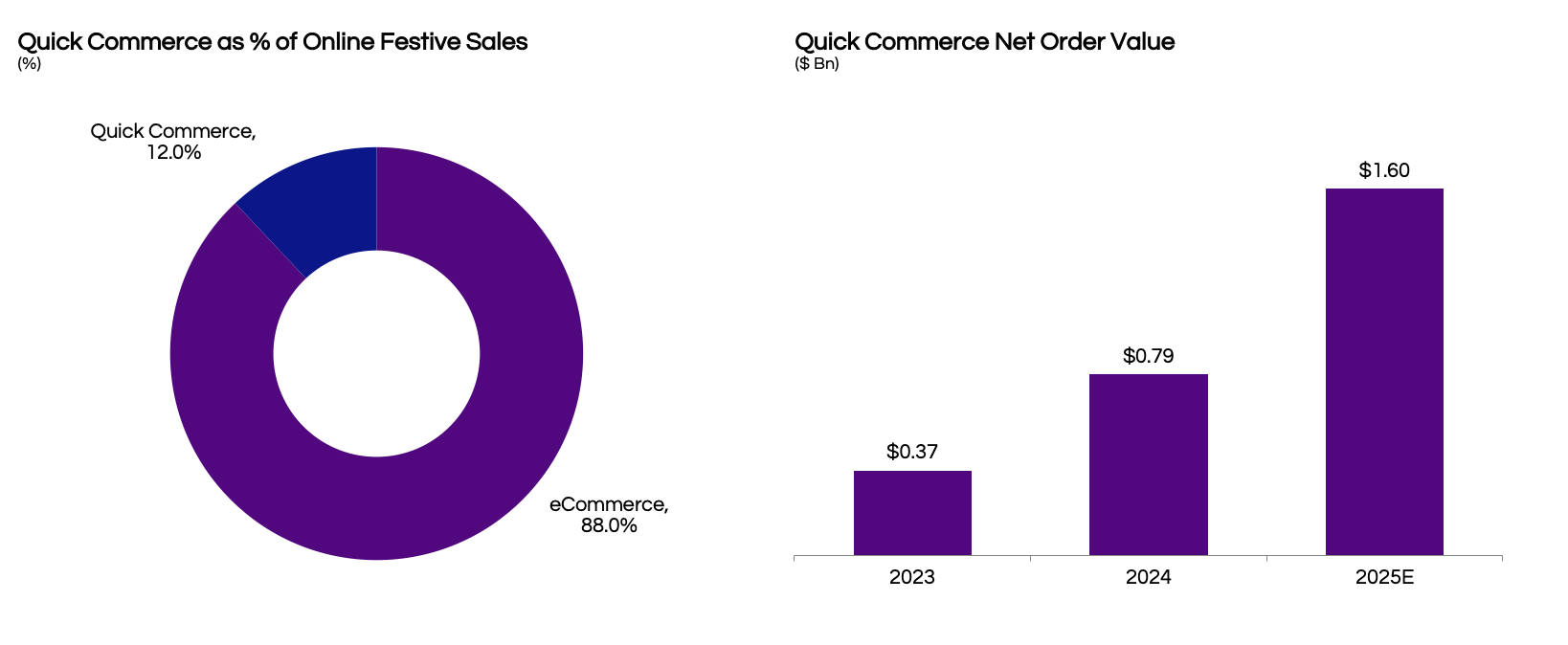

Quick Commerce to Account for 12% of Online Retail Sales up From 8% in 2024

Quick commerce is poised to play a significantly larger role in India’s festive e-commerce landscape in 2025. Its share of online festive sales is expected to jump to 12%, up from 8% in 2024, reflecting the growing consumer preference for instant deliveries and last-minute convenience during the shopping season.

This growth is mirrored in net order value, which has more than doubled year-on-year—from $0.79 billion in 2024 to an estimated $1.6 billion in 2025. With platforms like Blinkit, Zepto, and Swiggy Instamart expanding assortment and reach, quick commerce is no longer limited to groceries but is rapidly becoming a mainstream channel for festive gifting, beauty, personal care, and electronics accessories.

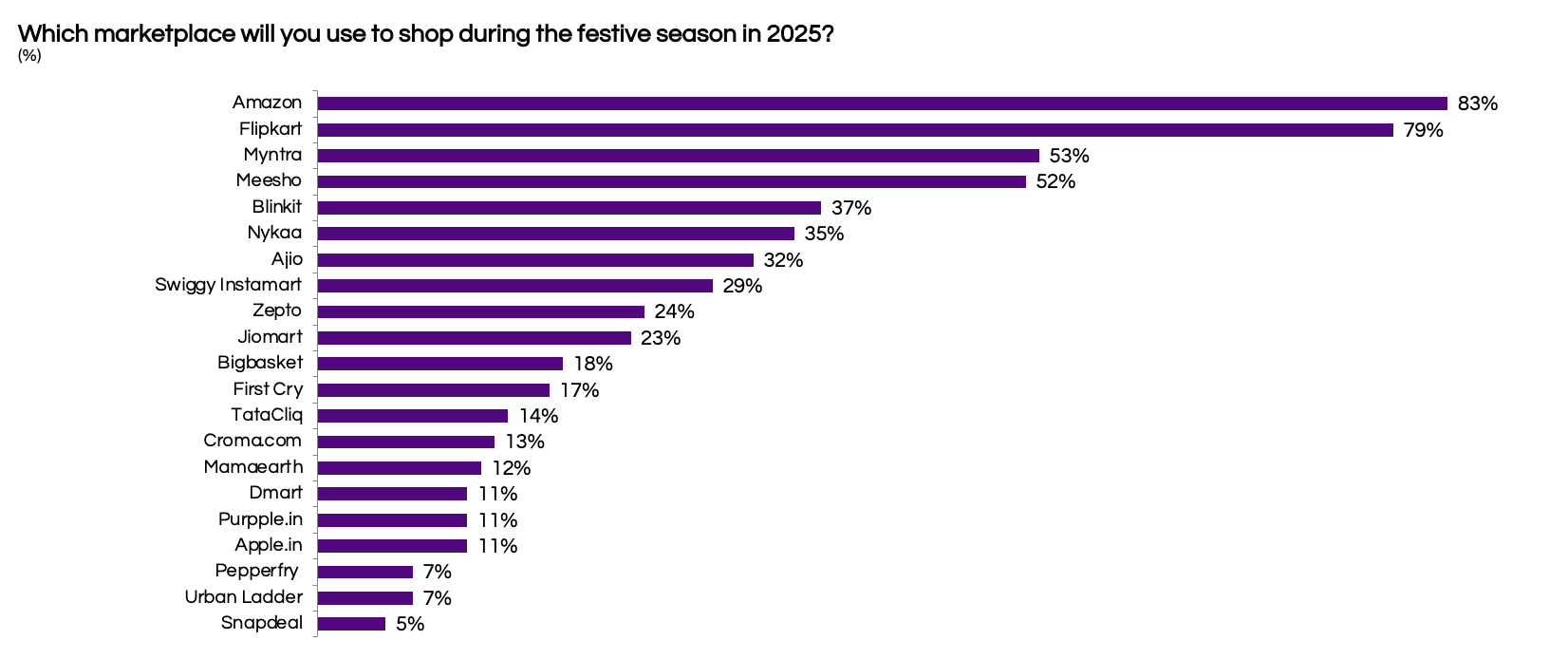

Amazon Preferred Platform Followed by Flipkart and Myntra

Amazon and Flipkart are set to dominate the 2025 festive season, with 83% and 79% of surveyed shoppers respectively planning to purchase from them. Myntra (53%) and Meesho (52%) are also major destinations, reinforcing their stronghold in fashion and value-conscious segments.

Notably, Blinkit (37%) has jumped into the top five ahead of Nykaa, signaling the rapid rise of quick commerce platforms in festive baskets. Emerging platforms like Ajio, Instamart, and Zepto continue to gain traction, reflecting an increasingly diversified ecommerce landscape.

Research Objective & Methodology

Research Objective: To understand the shopping behaviour of Indian consumers in the upcoming festive season

Festive Season: Starting from the first day of Big Billion Days/Great Indian Festival to 23rd October (Diwali)

Research Method: Online survey conducted 2,000 online adults across 20 cities in India between 10st August to 20th August 2025

{kind=link}